Table of Contents

- Q1: What are the differences between subscription access? (5500 only vs 5330 add on)

- Q2: Do I need the 5500 module to access 5330 e-filing?

- Q3: What is the purpose of the additional pages for the Schedule C P4/5?

- Q4: Why is the e-file status link disabled?

- Q5: If we discontinue access to the 5330 Add-on, will the filing history be lost?

- Q6: What is Form 8453-TE?

- Q7: What years are available for e-file?

- Q8: Do my clients need to get an additional credentials to use this service?

- Q9: What happens if a filing is rejected?

- Q10: Do filers have to physically print and sign the Form 5330?

- Q11: Do filers have to physically print and sign the Form 8453-TE?

- Q12: Do clients have to provide banking information?

- Q13: Is banking information stored?

- Q14: Will Batch processing be available?

- Q15: Can I file on behalf of my client through the portal?

- Q16: Will we be able to file on behalf of clients in the future?

- Q17: Are additional credentials needed to file on behalf of clients?

- Q18: What time zone is used when the IRS reviews submissions for timeliness?

Q1: What are the differences between subscription access? (5500 only vs 5330 add on) Top

5500 module subscribers:

- You can use multiple Form 5330s within the 5500 module.

- Draft forms are updated for e-filing, including:

- Updated address fields for the

- Filer

- Sponsor

- Paid Preparer

- Schedule C Page 5 Line 5b

- Extra pages for prohibited transactions and Schedule C entries.

- Updated address fields for the

5330 Add-On module subscribers, will get additional features, including:

- The ability to attach documents to individual form filings.

- 8822-b

- Amended Return Changes (template provided)

- Prohibited Transactions Correction Statement

- Prohibited Transactions No Correction Statement (template provided)

- Reasonable Cause Explanation

- The option to lock individual Form 5330s and invite the filer to e-file via the portal.

- E-filing includes:

- Submission of Form 5330.

- Automatic creation and completion of Form 8453-TE (required attachment). The form includes an option to authorize the IRS to withdraw taxes due. If selected, payment info is sent at the time of filing.

- A status dashboard at the plan level will allow you to track filing details including the pertinent dates, filing status, confirmation number, and the ability to amend filings.

Q2: Do I need the 5500 module to access 5330 e-filing? Top

Yes, a 5500 Module subscription is required to access the 5330 Add-On Module. Only forms created in the 5330 section of the 5500 Module will be available for e-filing.

Q3: What is the purpose of the additional pages for the Schedule C P4/5? Top

Additional pages were included to capture any transactions on Schedule C that didn’t fit in the available spaces. Since the Modernized e-Filing (MeF) system only permits certain attachments, these entries must be completely included within the form.

Q4: Why is the E-file Status Link disabled? Top

The E-file Status Link is enabled as soon as the e-filing capabilities are live for that specific filing year. Please Note: the 5330 e-filing options are only available for filing years 2023 and later.

Q4a: I can view the E-File Status dashboard, but can't lock or e-file. Top

The E-file Status dashboard is available to all users, but only those who subscribe to the 5330-Add on module are able to lock filings or submit them for e-file. Please Note: the 5330 e-filing options are only available for filing years 2023 and later.

Q5: If we discontinue access to the 5330 Add-on, will the filing history be lost? Top

Users that cancel their subscription will be able to see the filing status of the completed 5330 forms.

- Any forms that were filed electronically will be locked down and users will be unable to make changes.

- E-filing will not be available once the module is discontinued. Users will be able to unlock forms that were not e-filed, but after doing so they will remain in an unlocked status and e-filing will be unavailable.

Q6: What is Form 8453-TE? Top

The Form 8453-TE, found in the "Final" column of each Form 5330 filing, serves as a declaration of electronic filing with required signatures and details. This non-editable form auto-populates using information from the Form 5330 and user responses during submission. It is a mandatory attachment for all Form 5330 electronic filings.

Key Functions Include:

- Signature Authorization: It provides the electronic signature needed to validate the e-filing of Form 5330.

- Acknowledgment of Filing: It confirms that the taxpayer has reviewed the form and agrees to its contents.

- Payment Authorization (if applicable): It ensures that the IRS has permission from the filer to withdraw the excise taxes owed from the specified account on the agreed date.

Q7:What years are available for e-file? Top

E-filing for Form 5330 through ftwilliam.com is available for tax years 2023 and forward. According to Publication 4163, section 1.4.1, the IRS only accepts e-filed Form 5330 for the current and prior two tax years, meaning that as of 1/1/2026, only filings for 2023, 2024, and 2025 will be accepted. If you need to file for 2022 or earlier, you must file on paper, and no waiver is required. Users must wait for form years to be available in order to e-file (i.e. 12/31/2026 PYE filings may not be e-filed until the 2026 forms are available).

On the ftwilliam.com platform, the forms for 2023, 2024, and 2025 are specifically coded for those years. While the IRS accepts 2022 e-filings, our software cannot be used to submit them. Attempting to enter data for prior or subsequent years will result in a rejected or failed submission.

Q7a: What form year should I use for off calendar plan Form 5330 e-filings? Top

While the Form 5330 is not a year-specific form, the IRS requires that e-filed returns use a specific schema version tied to a form year. The IRS limits which plan year end dates are allowed for each form version through its e-file schema and business rules.

When e-filing Form 5330, the form year is based on the year end in which the excise tax applies. This date may vary depending on the section of Form 5330 being completed, and may be based on the end of the plan year, tax year, or calendar year. When selecting the filing year in the software, choose the year that matches the relevant year-end date.

NOTE: The IRS groups plan year end dates into filing years that run:

- December through the following November, not January through December.

- In simplest terms, any Form 5330 with a plan year-end date that falls before December 31 uses the prior year’s form

Please see the chart below to help determine the correct year to select in the ftwilliam software.

|

Year End Date Range of Filing

|

Form Year to Select |

|---|---|

| 12/31/2023 - 11/30/2024 | 2023 Filing Schema |

| 12/31/2024 - 11/30/2025 | 2024 Filing Schema |

| 12/31/2025 - 11/30/2026 | 2025 Filing Schema

|

|

NOTE: This guidance is intended to help you select the correct year within the ftwilliam.com software only, and does not impact the due date of the filing. Please refer to the Excise Due Date Table for specific filing deadlines.

| |

Q8: Do my clients need to get an additional credentials to use this service? Top

No, since your client is the filer and authorizes the transmission through the portal, they don’t need extra credentials. Please Note: Only the employer, individual, or other entity who is liable for the tax may file through the portal.

Q9: What happens if a filing is rejected? Top

According to Publication 4163, when a return is rejected, there is a 10-calendar day “Transmission Perfection Period” to fix and resubmit the return electronically.

This period is solely for correcting errors and does not extend the filing deadline. The 10-calendar day Perfection Period applies regardless of when the return was filed, whether before, on, or after the due date, including any extended due date. The IRS annual system maintenance (cutover period) does not extend the 10-day Perfection Period. This period is never extended.

- The chart below shows examples of how the IRS determines received dates, assuming:

- The first rejection occurred on the transmission date.

- The second rejection occurred on the re-transmission date.

- Acceptance occurred on the final transmission date.

NOTE: The 10-day Perfection Period is separate from filing deadlines and applies independently of when the return was submitted.

| Tax Year End | Due

Date |

Extension | E-Postmark

1st reject |

Original Trans.

1st Reject Date |

E- Postmark

2nd Reject |

Postmark 2nd

Reject 2nd Transmission/ Reject Date |

E-Postmark

Accepted Return |

Accepted Date/

Final Transmission |

IRS Received

Date |

| 12/31 | 3/15 | No | 3/9 | 3/10 | 3/10 | 3/12 | 3/29 | 3/30 | 3/29 |

| 12/31 | 3/15 | No | 3/9 | 3/10 | 3/10 | 3/12 | 3/19 | 3/20 | 3/9 |

| 12/31 | 3/15 | No | 3/14 | 3/15 | 3/23 | 3/24 | 3/24 | 3/25 | 3/14 |

| 12/31 | 3/15 | No | 3/9 | 3/10 | 3/15 | 3/15 | 4/3 | 4/4 | 4/3 |

| 12/31 | 3/15 | No | 3/9 | 3/10 | 3/14 | 3/15 | 3/23 | 3/25 | 3/14 |

| 12/31 | 3/15 | Yes

9/15 |

8/8 | 8/10 | 8/10 | 8/11 | 9/17 | 9/18 | 9/17 |

| 3/31 | 6/15 | Yes

12/15 |

8/10 | 8/10 | 12/22 | 12/23 | 1/9 | 1/10 | 1/9 |

| 3/31 | 6/15 | Yes

12/15 |

N/A | 8/10 | N/A | 12/23 | N/A | 12/28 | 12/23 |

| 12/31 | 3/15 | Yes

9/15 |

N/A | N/A | N/A | N/A | 9/30 | 10/1 | 9/30 |

* The IRS reviews the Electronic Postmark of the Accepted Return in determining the IRS Received Date.

- If there is not a rejected return within 10-calendar days of the Electronic Postmark of the Accepted Return, then the IRS Received Date will be the same as the postmark.

- If there is a rejected return within 10-calendar days of the Electronic Postmark of the Accepted Return, the IRS Received Date will be the earliest reject date within that 10-day period.

Explanation Example from chart:

- Row 1: The Electronic Return Postmark Accepted Return date shows 3/29. As the last rejected electronic postmark was 3/10, this falls outside of the 10-calendar day period, thus the IRS Received Date is recorded as 3/29.

- Row 2: The Electronic Return Postmark Accepted Return date shows 3/19. The earliest rejected electronic postmark that falls within the 10-calendar day period is 3/9. As such, the IRS received date is 3/9.

NOTE: Corrections must be submitted in the same format as their original filings. If the taxpayer is required to file their original return electronically, then they must also e-File their amended returns. A taxpayer must receive an approved waiver to file those tax years on paper. Information about requesting a waiver can be obtained by contacting the MeF Helpdesk at 1- 866-255-0654 or at IRS.gov.

Q9a: Known MeF Rejection Errors, Section B and Section E Top

There is a known issue with the MeF system when e-filing Section B or Section E as outlined below.

-

Section B. Taxes that are reported by the 15th day of the 10th month after the last day of the plan year.

Section B, reviews entries in Schedule D, Schedule E, Schedule F, and Schedule L.

When the submission includes entries for Schedule F, Line 1c, the value reported should be the greater of Line 1a or Line 1b multiplied by 5%. (As shown in the example below, Line 1b ($200), is greater than line 1a ($100). Line 1b $200*5%= $10)

While the system correctly calculates the value on Line 1c, the IRS response shows the filing as Rejected with the following error message:

Error: If ‘FailureMeetRqrEndngrCrtclTxGrp’ in Form 5330. Schedule F has a value, then ‘FailureMeetRqrPlnEndngrCrtclTxAmt’

must have a non-zero value equal to the greater of (‘ContriMeetBenchmarkOrRqrAmt’ and ‘AccumulatedFundingDefnAmt).

The IRS is aware of this issue and is working on a correction to suppress the error message and allow the filing. As of Feb. 2025, the filings are still being rejected. These will need to be paper filed until the IRS updates their software.

-

Section E. Tax that is reported by the last day of the month following the month in which the failure occurred.

Section E requires users to complete Schedule J, where the fee is calculated by multiplying the number of failures listed on Schedule J, Line 4, by $100. (As shown in the example below, Line 4, 30 failures * $100= $3,000.00)

While the system correctly calculates the value on Line 5, the IRS response shows the filing as Rejected with the following error message:

Error: If Form 5330, Schedule J, 'FailProvideNtcRedFutAccrTaxAmt' has a value,

then it must be equal to 'TotERISASect204hNtcFailureCnt' multiplied by 100.

The IRS is aware of this issue and is working on a correction to suppress the error message and allow the filing. As of Feb. 2025, the filings are still being rejected. These will need to be paper filed until the IRS updates their software.

Q9b: Known MeF Rejection Error: "PaymentAmt must not be greater than 200% of TaxDueAmt." Top

Although Form 8453-TE allows filers to report Form 5330 tax amounts in dollars and cents, the IRS payment processing center only accepts whole dollar amounts. This discrepancy has not yet been resolved in the IRS systems to accommodate returns where the tax due may be less than $1.00

How the Error Occurs:

- When the reported tax on Line 19 is between $0.01 and $0.49, during the payment process, the system rounds the amount to $1.00.

- Since $1.00 is more than 200% of any amount below $0.50, the IRS rejects the filing under their payment validation rules.

IRS Guidance:

According to IRS representatives from the Modernized e-File (MeF) team, filers have two options to resolve this issue:

- Round Up the Tax Amount

Adjust the tax reported on Line 19 of Form 5330 to at least $1.00, then submit the payment electronically. -

Decline Payment During E-Filing

Submit the return without payment. If the IRS later issues a letter requesting payment, the filer can:- Pay the amount at that time.

- Include an explanation for why payment was not submitted with the return.

- Attach the IRS rejection notice as supporting documentation.

Q10: Do filers have to physically print and sign the Form 5330? Top

Filers are required to retain copy of the Form 5330 for their records, but a copy of a manually signed 5330 does not need to accompany the filing. For subsequent steps to be completed in the Portal, the filer must first select the Print 5330 button.

Q11: Do filers have to physically print and sign the Form 8453-TE? Top

Filers must include a signed Form 8453-TE with each filing. This can be done using a digital/electronic signature or by printing and wet signing the form and uploading it as a PDF within the signing process. For details on digital/electronic signatures, refer to IRS Electronic Signature Program (Section 10.10.1.6.2 and Exhibit 10.10.1-2).

Q11a: Does the 8453-TE signer need to be the same individual as the 5330 filer? What should be done if the Officer is different from the person responsible for the tax? Top

The filer listed on Form 5330 does not have to be the same person as the officer listed on Form 8453-TE.

- Form 5330: The filer on Form 5330 is typically the person or entity responsible for filing the form, which could be the organization itself or a tax professional.

- Form 8453-TE: The individual who signs the 8453-TE must be either the person responsible for the tax or an officer of the tax-exempt entity.

- If signing as an Officer, that person must be someone who has the authority to sign on behalf of the organization (like the president, vice president, or treasurer).

- Again, the signer does NOT have to be the same person who is listed as the filer on Form 5330.

The distinction is made in Part II paragraph 3 on the 8453-TE by selecting the applicable check box:

Q11b: Does Part III of the Form 8453-TE need to be completed by the Paid Preparer (or ERO)? Top

No, when using the ftwilliam.com software and filing Form 5330 through the portal, Part III of Form 8453-TE does not need to be completed by the ERO or the paid preparer. Even if a paid preparer or ERO helped prepare the form, the actual filer is the one submitting it electronically, so this section does not apply.

Q12: Do clients have to provide banking information? Top

Filers have the option to opt out of submitting payment at the time of e-filing. If they choose this option, they will be responsible for providing payment outside of the ftwilliam.com software.

Update (February 2026): Based on customer feedback, the 5330 ACH debit will debit the client's bank account as: IRS USATAXPYMT.

Update (May 2025): Based on customer feedback, filers who either choose not to submit payment at the time of filing, or whose payment is declined due to inaccurate information will need to send a check or money order with the following information:

Payable to: The United States Treasury

Include:

- Your Tax ID (EIN or SSN).

- Tax form number.

- Tax period

- Mail to:

- Internal Revenue Service

- PO Box 1211

- Charlotte, NC 28201-1211

NOTE: We are only able to provide the following information and cannot offer additional guidance beyond these details.

Q13: Is banking information stored? Top

Banking information is not stored. After a filing is submitted, payment details are deleted, leaving only a Yes or No indicator of whether payment information was sent. Filers are encouraged to carefully verify banking details before submitting.

Q14: Will Batch processing be available? Top

In the second release phase (TBD) users will be able to batch edit check, lock, and invite portal users to e-file as well as review the status of filings within the batch. More details to come.

Q15: Can I file on behalf of my client through the portal? Top

Only the employer, individual, or other entity who is liable for the tax may file the 5330 through the portal. Please see Q16/17 pertaining to filing on behalf of clients.

Q16: Will we be able to file on behalf of clients in the future? Top

We are investigating options pertaining to users filing on behalf of their clients but do not have an ETA on if or when this will be available. If implemented, the functionality will be similar to the 5500 module sign on behalf of feature. More details to come.

Q17: Are additional credentials needed to file on behalf of clients? Top

Yes, if implemented in the future, all electronic filers filing on behalf of clients, must register as an Electronic Return Originator (ERO).

Please note that the application process may take up to 45 days for approval.

The IRS outlines this process in 3 steps:

We have also included a detailed tutorial on the application process: Creating Your Application to Become an Authorized IRS e-file provider.pdf

Q18: What time zone is used when the IRS reviews submissions for timeliness? Top

The IRS Received Date is initially set by the electronic postmark in the Transmitter’s time zone (Central Time for ftwilliam.com). If there’s a question about timeliness and the Transmitter is in a different time zone, the taxpayer’s time zone will determine the received date.

Form 5330 Attachments – What to Attach and How

When filing Form 5330, certain situations require additional documentation. This page explains each attachment type, when to use it, and how to prepare it correctly.

Use the attachment type that best matches your filing scenario.

- 8822-B

- Amended Return Changes (template provided)

- Binary Attachment

- Prohibited Transactions Correction Statement

- Prohibited Transactions No Correction Statement (template provided)

- Reasonable Cause Explanation

NOTE: Attachments may be added and removed from individual form filings by selecting the Attachment link below the specific form listing in the 5330 section:

8822-B: Change of Address or Responsible Party (Return to top)

Format

- PDF file (IRS Form 8822‑B)

Purpose

- Notifies the IRS of a change to a business address or responsible party.

Instructions

- Complete IRS Form 8822‑B located under the Other Forms section (below the 5330 section of the 5500 Module)

- Save the completed form as a PDF by selecting the Form 8822-B link under the Final column

- Attach the PDF to your Form 5330 filing

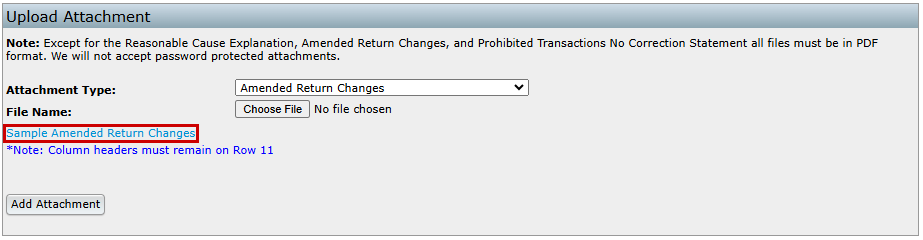

Amended Return Changes (Return to top)

Format

- CSV spreadsheet- template provided on Attachments page

Purpose

- Required when filing an amended Form 5330

- Explains what values changed and why

Instructions

- Download and complete the provided .CSV template

- All columns must be completed

- Do not edit or remove the header row or rows 1–11, as this will prevent the file from importing properly

Template Guidance

- PartNum – Enter I (Part I, Lines 1–16) or II (Part II, Lines 17–19)

- LineNum – Enter the Form 5330 line number being corrected

- OnPreviousReturnAmt – Amount reported on the original return

- OnAmendedReturnAmt – Corrected amount

- ExplanationTxt – Brief explanation of the change

NOTE: Changes to schedules on pages 3–6 of Form 5330 do not need to be documented.

Example

- Completed CSV showing original vs. corrected amounts

Binary Attachment (Return to top)

Format

- PDF file

- Password‑protected files are not allowed

Purpose

- Used for supporting documentation that does not fit another attachment type

Instructions

- Enter a descriptive attachment name (required field)

- Upload a PDF file only

Example

Reasonable Cause Explanation (Return to top)

Format

- Text entered directly into the attachment window

Purpose

- Explains why a filing was late, incorrect, or otherwise non‑compliant

- Supports requests for penalty relief

Instructions

- Enter the explanation directly in the provided text field

- The system converts the text into the required IRS format

- Keep explanations clear, concise, and specific

Example

Prohibited Transactions Correction Statement (Return to top)

Format

- PDF file

- Password‑protected files are not allowed

Purpose

- Used when prohibited transactions reported on Schedule C have been corrected

Instructions

- Create a PDF documenting each corrected transaction

- Upload the PDF with your Form 5330 filing

Required Information

- Transaction Number (from Schedule C, column (a))

- Description of the transaction

- Correction Date

- Correction Method (e.g., lost earnings deposited, loan re‑amortization)

- Excise Tax Paid

Example

- PDF listing corrected transactions with correction details and excise tax amounts

Plan Name: ABC Company 401(k) Plan

EIN: 12-3456789

Plan Year: 2024

Transaction 1:

- Transaction Number: 001

- Description: Late deposit of employee deferrals from January 2024 payroll.

- Correction Date: 03/15/2025

- Correction Method:

- The employer deposited the missing deferrals into affected participants' accounts.

- Lost earnings were calculated using the Voluntary Fiduciary Correction Program (VFCP) calculator and credited accordingly.

- Affected participants were notified of the correction.

- Excise Tax Paid: $2,000

Prohibited Transactions No Correction Statement (Return to top)

Format

- CSV spreadsheet- template provided on Attachments page

Purpose

- Used when prohibited transactions have not yet been corrected

- Reports planned correction dates not captured on Schedule C

Instructions

- Download and complete the provided .CSV template

Template Guidance

- TransactionNum – Transaction number from Schedule C (3 digit max- leading zeros may be removed)

- TransactionDesc – Brief description of the transaction

- PlannedCorrectionDt – Planned correction date (MM/DD/YYYY)

Example

| TransactionNum | TransactionDesc | PlannedCorrectionDt |

|---|---|---|

| 1 | Late deposit of January 2024 deferrals | 03/15/2025 |

| 2 | Incorrect loan offset distribution | 04/01/2025 |

Key Differences between Prohibited Transactions Correction Statement and Prohibited Transactions No Correction Statement(Return to top)

Feature |

Correction Statement |

No Correction Statement |

|---|---|---|

Purpose / When to Use |

Used to report corrected prohibited transactions. Required when a prohibited transaction has been corrected and needs to be reported to the IRS. |

Used to report unresolved prohibited transactions with a planned correction. Required when no correction has been made yet. |

Required Attachment Type |

PDF file (customer generated) |

CSV Spreadsheet (template provided) |

| Details Included | Includes detailed correction info:

1. Transaction Number from Schedule C 2. Description of the transaction 3. Correction Date (MM/DD/YYYY) 4. Correction Method (e.g., lost earnings, re-amortization, etc.) 5. Excise Tax Paid |

Includes unresolved transaction details:

1. Transaction Number from Schedule C 2. Description of the unresolved transaction 3. Planned Correction Date (MM/DD/YYYY) |